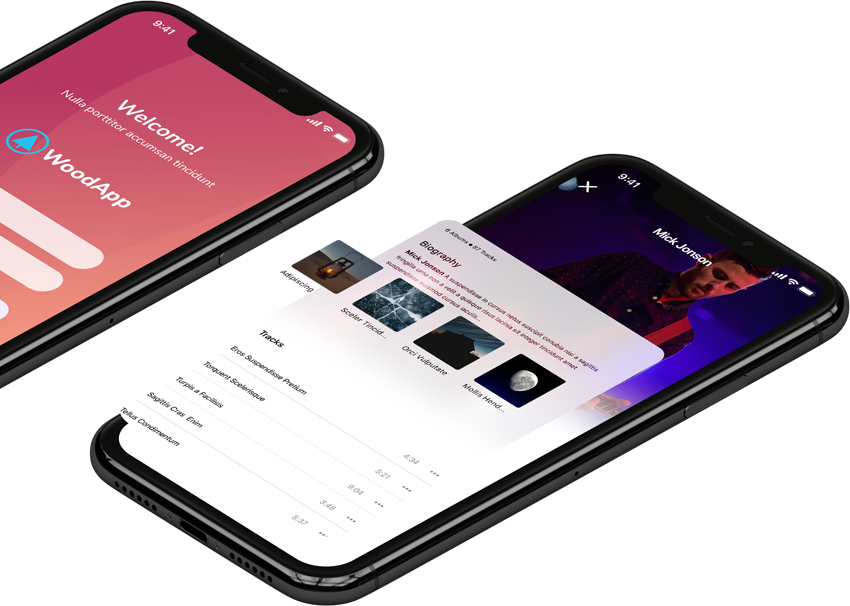

Instantly Verify Consumer Income & Employment Status

_Income API

Minimise credit risk by using our _Income API to verify consumer employment income and use that income for credit decisioning.

Make more profitable lending decisions whilst reducing credit risk

Using _Income API Mercury Enriched enables clients to fully automate verification for both income & employment. Effortlessly allowing clients to roll-out their KYC & AML processes in days, not months or years.

We take all of the hassle out of income verification by using machine-learning & instant biometric SCA to power _Income API.

- Complete UK, European & Australian Coverage

- Instant biometric SCA

- Automate income & affordability checks

- Effortless consumer onboarding

- Seamless KYC process automation

What is _Income API?

Built on top of open banking and the fastest financial rails, _Income API provides your customers with an effortless way to securely verify their income and employment.

Built for Developers. Built for Scale & Speed

We turn complex financial algorithms & infrastructure into simple API calls to save your team thousands of development hours.

Build quickly, scale effortlessly and go-to-market in days not weeks using Mercury Enriched APIs.

Income & Verification API Frequently Asked Questions

Income verification, affordability & creditworthiness are two central pillars of responsible & profitable financial decisioning.

Being able to accurately calculate affordability & creditworthiness allows clients to minimise their underwriting credit risk.

Affordability centres around the consumers ability to afford a new financial liability.

_Income API uses AI to analyse historical financial records to validate consumer income & employment, ensuring they would be able to comfortably afford their new loan, credit card, financed purchase and so on.

Creditworthiness centres around the consumers likelihood to meet new financial commitments.

Our _Income API makes automating consumer income & employment verification effortless.

It has been designed to ensure clients are always compliant & also save weeks of development time and costs.

_Income API Workflow

- Client generates a new _Income API session request with their new consumer estimate income and payment frequency

- End-user is sent an authorisation session link via SMS

- End-user provides access to their bank account via Open Banking

- End-user session & involvement ends at this point

- _Income API algorithms use AI to analyse end-user financial data for income and employment

- Client is returned _Income API analysis in JSON/Application format

{

"success": true,

"message": "Income data",

"code": "200",

"data": {

"monthly_income_summary": [

{

"income_value": "1450.42",

"income_check": "PASSED",

"month_end": "2021-11-30",

"primary_account_check": "PASSED",

"income_frequency": "MONTHLY",

"income_employer": "CLEVELEYS.COM"

},

{

"income_value": "1450.42",

"income_check": "PASSED",

"month_end": "2021-10-31",

"primary_account_check": "PASSED",

"income_frequency": "MONTHLY",

"income_employer": "CLEVELEYS.COM"

},

{

"income_value": "1450.42",

"income_check": "PASSED",

"month_end": "2021-09-30",

"primary_account_check": "PASSED",

"income_frequency": "MONTHLY",

"income_employer": "CLEVELEYS.COM"

},

{

"income_value": "1450.42",

"income_check": "PASSED",

"month_end": "2021-08-31",

"primary_account_check": "PASSED",

"income_frequency": "MONTHLY",

"income_employer": "CLEVELEYS.COM"

}

]

}

}

}

KYC means Know Your Customer and sometimes Know Your Client.

KYC or KYC check is the mandatory process of identifying and verifying the client’s identity when opening an account and periodically over time.

In other words, banks must make sure that their clients are genuinely who they claim to be.

Banks may refuse to open an account or halt a business relationship if the client fails to meet minimum KYC requirements

Why is KYC Essential

KYC procedures defined by banks involve all the necessary actions to ensure their customers are real, assess, and monitor risks.

These client-onboarding processes help prevent and identify money laundering, terrorism financing, and other illegal corruption schemes.

KYC process includes ID card verification, face verification, document verification such as utility bills as proof of address, and biometric verification.

Banks must comply with KYC regulations and anti-money laundering regulations to limit fraud. KYC compliance responsibility rests with the banks.

In case of failure to comply, heavy penalties can be applied.

Short Video About KYC

- Consumer Lending – Automate regulatory & compliance affordability checks whilst using accurate historical financial data to reduce credit risk.

- Commercial Lending – Get an instant snapshot of commercial health and creditworthiness using historical financial data delivered by _Affordability API

- Real Estate & Housing – Instantly determine whether a client can afford new mortgage and rental commitments based on their current and historic financial health.

Anti-Money Laundering, otherwise known as AML is a set of laws and compliance procedures, these aim to protect financial institutions from criminals using financial systems to launder money from criminal proceeds.

Short Video About Anti-Money Laundering (AML)

PSD2 otherwise known as, The Revised Payment Services Directive, is a European regulation for electronic payment services.

It seeks level the playing field between banks and non-banks, using the democratisation of data to increase competition & innovation.

Short Video About PSD2

Do clients have to assess affordability separately from creditworthiness?

Chapter 5 of the FCAs Consumer Credit sourcebook (CONC) outlines a requirement for clients to assess the creditworthiness of a customers. This is the customer’s ability to make repayments as they fall due, covering both affordability & creditworthiness.

So in essence, no – clients should be assessing affordability in a parallel with credit worthiness.

Does the FCA define how clients should check affordability & creditworthiness.

The FCA does not clearly define how clients should check the affordability & creditworthiness of customers.

The scope of all affordability assessments should cover the type and amount of credit, alongside the customer’s financial position.

A client is required to make a ‘reasonable’ assessment of a customer’s affordability & creditworthiness, our _Affordability API automates this process and provides with with a accurate historical & present assessment.

Do I have to use a credit reference agency (CRA) to make a creditworthiness assessment?

There is absolutely no requirement for our clients to use CRAs to make creditworthiness assessments. The Mercury Enriched _Affordability API provides the most accurate representation of a customer present & historic affordability & creditworthiness.